North Bay Real Estate Market Update - March 2023

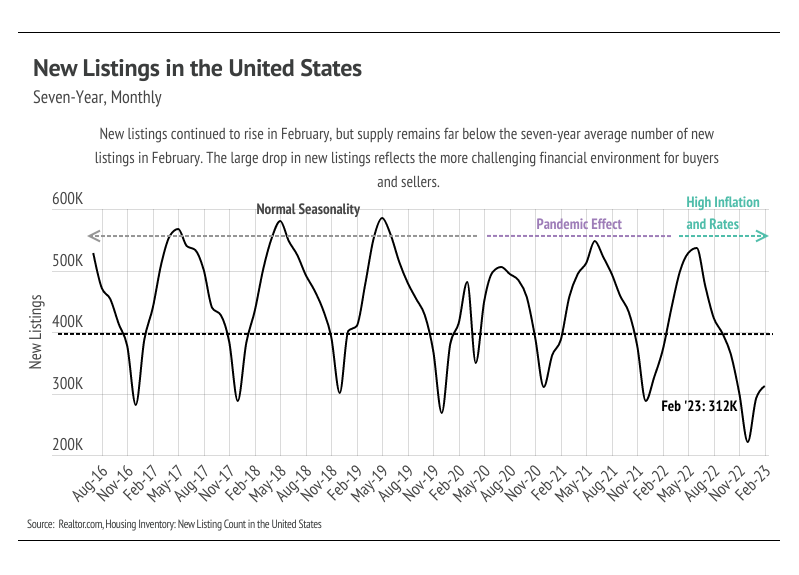

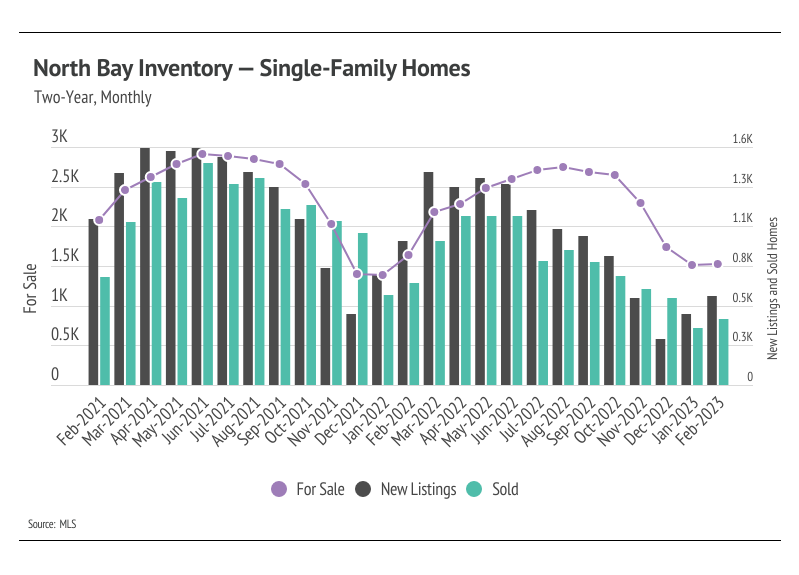

Single-family home inventory rose slightly month over month, as new listings outpaced sales, but far fewer listings came to market than is typical this time of year. Higher interest rates have dropped incentives for potential sellers to enter the market, since sellers usually also must buy a new home. Homeowners either bought or refinanced recently, locking in a historically low rate, which means they aren’t selling and fewer listings are coming to market. Moreover, many potential buyers were priced out of the market as interest rates rose; however, interest rates have been higher for enough time that buyers are more comfortable re-entering desirable markets like the North Bay. Currently, buyers aren’t facing anything similar to the hypercompetitive 2021 market, but we will likely start to see more competition in the spring. New listings fell by 37.2% year over year, while sales declined 33%. We still expect some inventory growth in the first half of 2023, but inventory will likely remain low.

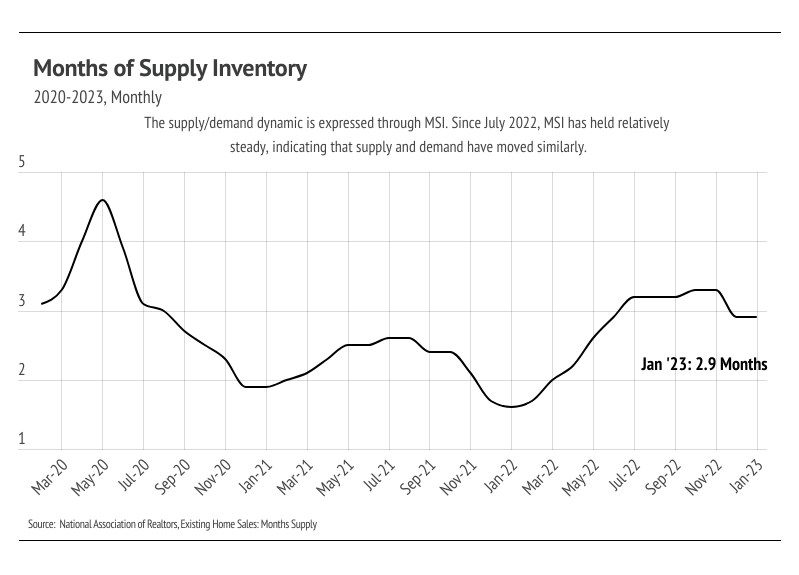

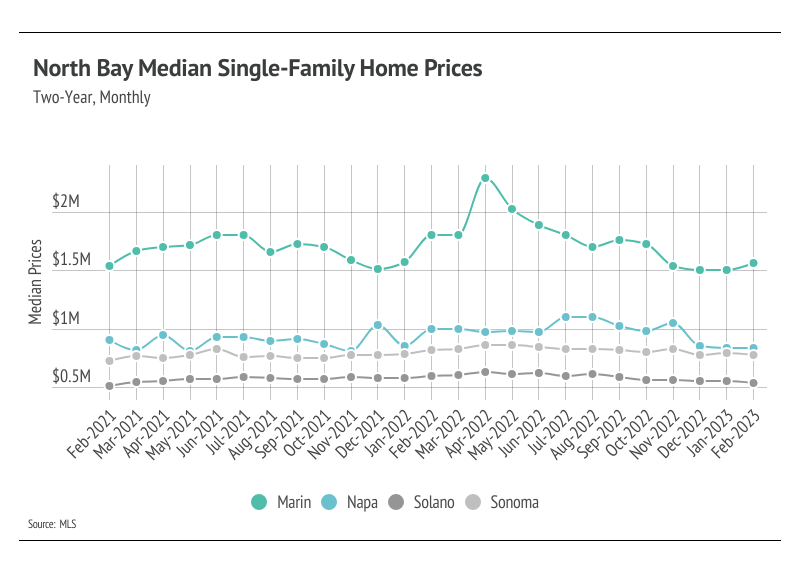

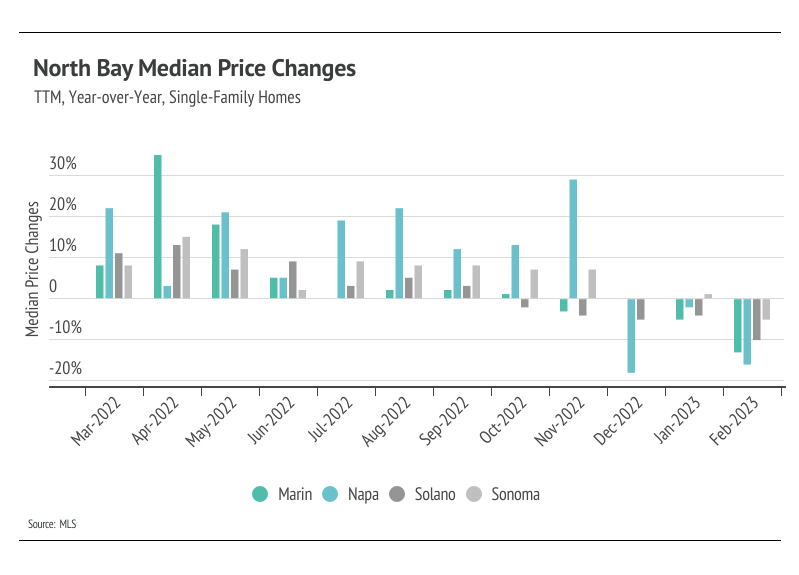

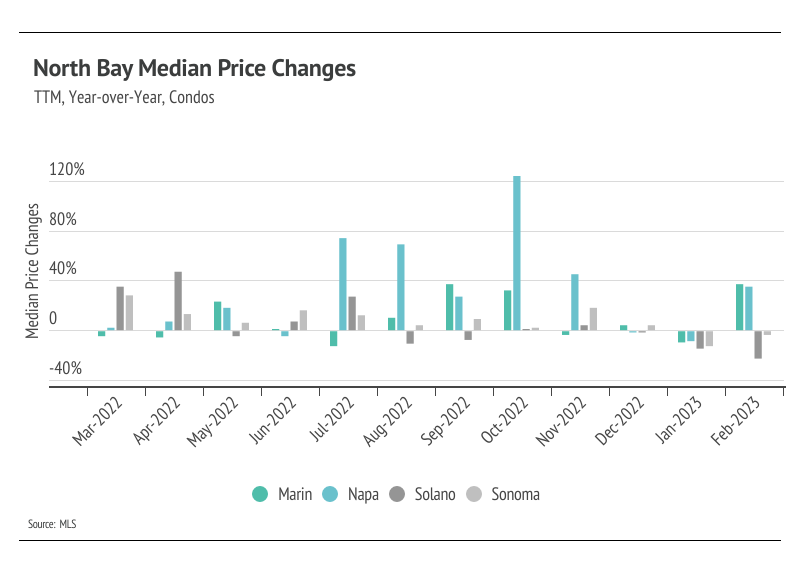

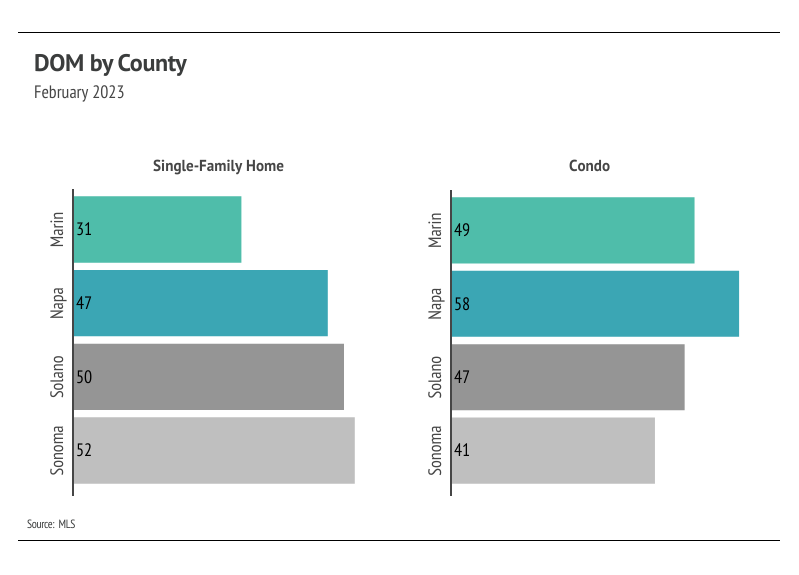

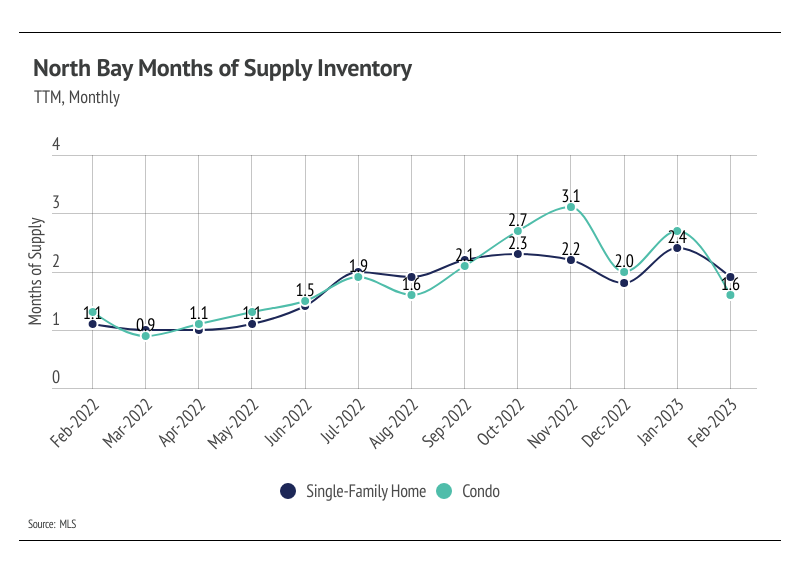

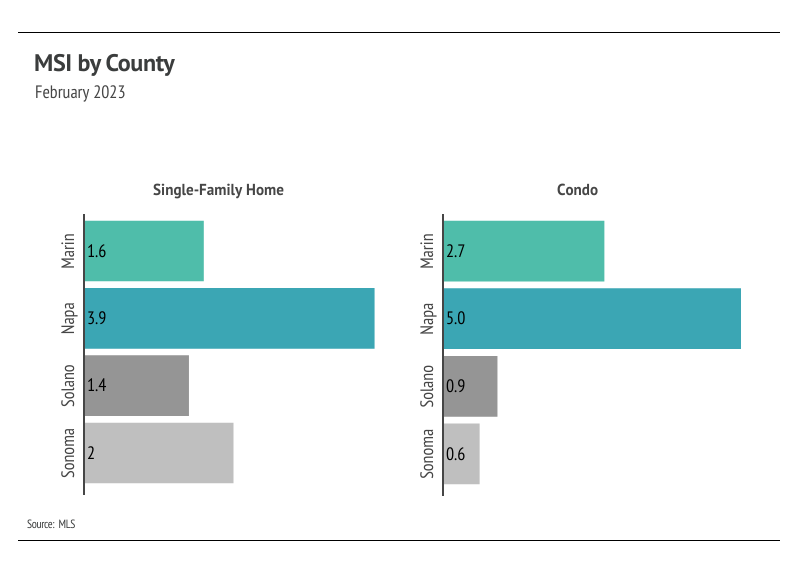

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI in the North Bay already indicated a sellers’ market, but dropped lower in February for both single-family homes and condos. Napa’s MSI, which implies a buyers’ market, is the one exception. The sharp drop in MSI occurred due to more sales and homes selling more quickly.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.